Q1 2026 Research Theme: Bottlenecks Slow Cloud-Based AI Data Centre Growth But Device-Embedded AI Is Powerful Alternative For Oil & Gas

- Mar 31

- 17 min read

Updated: Jun 8

Since we first wrote about AI some two years ago, the AI spend has gone through the roof – the hyperscalers are each spending substantially more than US$100 billion annually to build compute power! However, such explosive growth in AI spend has yet to be matched by sufficient on-grid or on-site power, gas-fired generation capacity included, coming onstream to address such AI-driven energy demand. Major multi-year supply chain and permitting bottlenecks are conspiring to delay, postpone, even cancel future on-grid & off-grid data centres. As a result, our risked estimate of likely near to medium-term incremental gas demand for U.S. data centres remains modest - particularly when compared with the burgeoning gas demand for U.S. LNG exports.

As enterprises and consumers increasingly adopt AI services, such as agentic AI, and AI-enabled devices, such as self-driving vehicles, a growing array of smaller ‘edge AI’ data centres will be required – close to cities, commercial and manufacturing centres etc. – to provide the real-time AI responses that users and devices require.

Such ‘edge AI’ data centres will prompt a broader geographic distribution of AI power demand, potentially reducing critical grid bottlenecks but major equipment and labour-related supply chain and permitting bottlenecks will remain.

We therefore do not expect this structural migration of AI workloads toward ‘edge AI’ data centres to fundamentally alter our modest AI-led projections for incremental near-term U.S. gas-fired generation capacity.

AI workloads can now migrate beyond ‘edge AI’ data centres to individual phones, tablets, or IoT devices that run small yet highly capable AI models even when offline - opening up a new world where the power of AI is at the very point of measurement, observation or request - providing well-informed intelligent decisions in real-time.

Local or device-embedded AI is fast emerging as a powerful alternative to cloud-based AI for oil & gas operations. Running intelligent ‘edge AI’ analytics close to operating assets enables intelligent, real-time decisions, ensuring swift identification and response to any issue that may threaten operational efficiency, asset integrity, personnel safety or the environment.

Minimum AI Table Stakes Now Top US$100 Billion

Upon rereading our first research note about AI, ‘Gen AI Will Transform the Oil & Gas Sector’, published in early 2024, several quotes leap off the page:

‘Alphabet, Meta and Microsoft alone are forecast to spend a staggering US$140 billion on Gen AI this year; Amazon likely takes this annual spend up to near US$200 billion.’

‘…. Big Tech continues to commit tens of billions of dollars to Gen AI ….’.

Two years on, such numbers no longer move the needle: US$140 billion, even US$200 billion, of aggregate annual AI spend is no longer staggering in today’s world. And, to paraphrase 1990s supermodel Linda Evangelista, committing tens of billions of dollars to Gen AI is frankly ‘not worth waking up for’!

The minimum stake to sit at the AI table is now upwards of US$100 billion and will likely increase further with time.

‘Harder, Better, Faster, Stronger’ - The AI Arms Race Continues Apace

‘Work it harder, make it better, do it faster, makes us stronger’ - the lyrics of Daft Punk’s 2001 anthem appear somewhat prescient given the intense rivalry between the Big-5 U.S. hyperscalers (Big-5) - Amazon, Alphabet, Microsoft, Meta and Oracle - and AI companies such as Anthropic, OpenAI and xAI as they all race to deliver larger, faster, better AI models.

Progress is now measured in trillion-parameter LLMs (large language models), multi billion-dollar data centre campuses and multi-gigawatt power draws (enough to power a major metropolitan area!).

The hyperscalers are in a race to develop AGI – artificial general intelligence - AI capable of performing any intellectual task at or above human level. Such ambitions are already enabling Agentic AI - AI that can autonomously plan and execute complex tasks – reinforcing the need for ever more specialised compute power.

It is worth noting that a growing number of industry insiders and observers openly question whether LLMs alone - no matter how large - can ultimately deliver true AGI. The jury is out but right now the hyperscalers are betting heavily that ever-larger LLMs and data centres will get them there.

The Big-5 Are Now Spending Close To US$2Billion A Day !

Amid this AI boom, compute power has become one of this decade’s most critical resources.

The sheer scale and rate of growth of US-led AI infrastructure boggles the mind. Aggregate 2026E capital expenditure of US$700bn-plus by the Big-5, represents the largest annual technology-focussed investment in history, accompanied by a jaw-dropping 90% CAGR surge in such expenditure since 2024.

Furthermore, a growing number of investment banks - Bank of America, Goldman Sachs, Morgan Stanley et al - foresee global AI capital expenditure breaching US$1 trillion by 2027!

McKinsey’s own research1 shows that by 2030, data centres are projected to require over US$5 trillion worldwide to keep pace with the demand for compute power.

That is a genuinely staggering number by any measure? But check back in a couple more years!

1McKinsey Data Centre Demand Model, McKinsey Data Centre Capex TAM Model, expert interviews

Big-5 Spend on AI Infrastructure, 2024 - 2026E

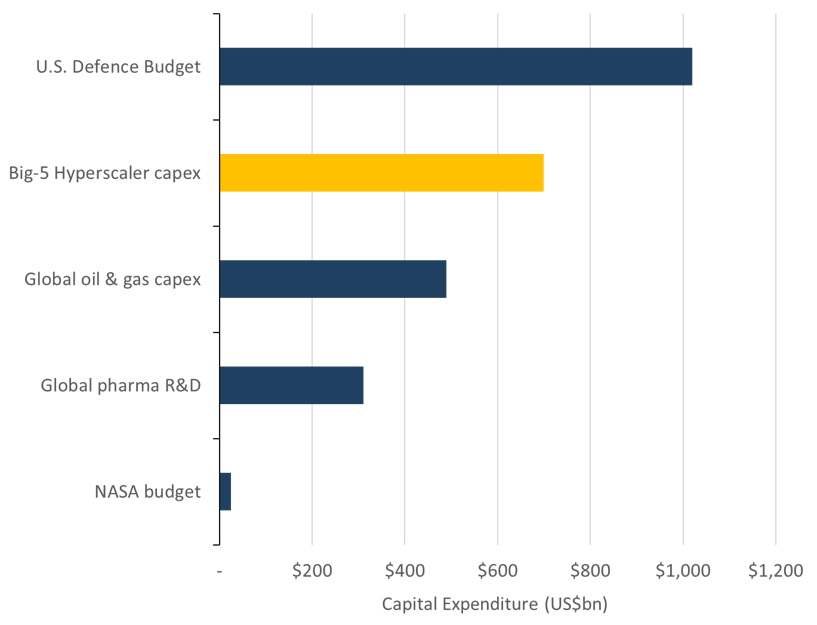

To put such spending in perspective, forecast 2026 AI capex by the Big-5 alone exceeds that of both global oil & gas capex and global pharmaceutical R&D, standing second only to the gargantuan U.S. defence budget.

2026E Big-5 Capex vs. Other U.S. & Global Industrial Sectors

Moreover, Big-5 capex for 2026E alone is near three-fold the inflation-adjusted cost of the entire Apollo Program, twenty-fold that of the Manhattan Project!

Before we go any further, it is also worth comparing the AI spend of U.S. technology companies with that of non-US AI companies across both Europe and Asia.

At US$700bn, the Big-5 will spend almost seven-fold as much on AI infrastructure and GPU chipsets as their Chinese counterparts, according to Morgan Stanley.

Since 2013, according to the Stanford HAI 2026 AI Index, investment in privately-held U.S. AI companies has reached almost US$760 billion, six-fold the capital raised by their Chinese counterparts, with the U.K. a distant third at just US$34 billion!

Money alone does not ensure AI success: after all, necessity is the mother of innovation. U.S. export restrictions on advanced GPU chips forced Chinese AI firms to focus on algorithm improvements. DeepSeek-R1, a Chinese AI model released early 2025, matched top-tier U.S. AI model performance despite using older, less capable GPU chips. The U.S.-China AI model performance gap has closed according to the Stanford report cited above - Anthropic’s latest AI model outperforms the best Chinese AI model by < 3%. |

This unprecedented, US‑led AI capex cycle is not just a technology story; it is reshaping long‑term demand for power, gas infrastructure and grid equipment.

Where’s All The Power Going To Come From Given Huge Grid Connection Delays?

As the U.S.-led AI boom drives demand for ever more computing power, data centre developers struggle to keep pace, largely because securing timely access to the scale of reliable, high-capacity grid power required to run such facilities has become so challenging.

Data centres now face at least four years to access grid power due to permit delays and the necessary upgrades to local grid infrastructure. Moreover, data centre-driven power demand can destabilise regional electricity grids, driving up residential power pricing.

A dozen U.S. states, including data centre ‘capital’ Virginia, have thus proposed temporary moratoriums on large new grid-fed data centres but none have yet passed into law.

White House Executive Order 14318 of mid-2025 aims to accelerate federal permitting of new data centres by up to 18 months but cannot mitigate the required grid upgrades.

Data Centre Developers Are Scrambling For On-Site Gas-Fired Power Generation …

With a growing pipeline of ‘gigawatt-scale’ data centres, developers are scrambling for ‘behind-the-meter’ onsite power solutions, notably gas-fired generation capacity.

Some 95GW or 38% of gas-fired capacity in development - either under construction, pre-construction or merely announced - is destined for onsite power for data centres, essentially a new gas market given the negligible onsite commitments of 2024.

Overall U.S. gas-fired capacity in development has near-tripled to over 250 GW year-on-year. But bear in mind that total operational U.S. gas-fired power capacity stands at ca. 575GW.

U.S. Gas-Fired Power Plant Capacity In Development* Has Tripled Year-on-Year

A third of U.S. data centres could be fully operating off-grid by 2030, according to a study by Bloom Energy. Such strategic moves by developers are inevitably steering future large-scale data centre investment toward energy-rich states such as Texas, Louisiana and Pennsylvania that possess significant gas resources - as the map below clearly demonstrates.

Location Of Planned New US Gas-Fired Power Generation Plants

… But Major Equipment Delays Are Also Slowing Off-Grid Data Centre Projects

Data centre developers are truly caught between the devil and the blue sea: their scramble for off-grid power clearly avoids the grid-related delays detailed earlier but they still remain exposed to a host of supply chain bottlenecks for vital off-grid power-related equipment, notably turbines, medium and low-voltage transformers and switchgear.

Gas turbine manufacturers’ delivery lead times already extend through 2030. Indeed, two-thirds of gas power projects in development cannot yet confirm their turbine supplier!

High-voltage transformers - with lead times upwards of three years - are already a critical bottleneck for prospective grid-powered data centres. But, as more data centres migrate toward off-grid power, so the lead times for typical medium and low-voltage transformers have surged in tandem to over two years.

Significant U.S. tariffs on Chinese transformers have heavily impacted the supply chain for U.S data centres. China controls over 60% of the global transformer manufacturing capacity.

Near-Term Incremental Gas Demand For Off-Grid U.S. Data Centres Will Remain Muted

The Big-5-fueled data centre boom faces a harsh reality: chronic shortages of skilled labour, critical power and electrical equipment alongside bureaucratic permitting delays.

Headlines speak of up to half of planned data centre projects facing delays or indeed cancellation. Just a fraction will therefore come to fruition on budget and on time as developers navigate the stark reality of permitting, supply chain bottlenecks and construction delays.

Of the 252 GW of gas-fired power generation capacity in development, 95 GW (38%) is earmarked for on-site power generation; 30 GW is under construction, 160 GW is ‘pre-construction’ and the remaining 62 GW merely ‘announced’.

Excluding all ‘announced’ gas-fired projects and applying a 50% haircut to ‘pre-construction’ projects yields a risked incremental power load of 110 GW, including ca. 40 GW of on-site capacity, the latter requiring incremental on-site gas demand of ca. 5 bcf per day.

Assuming 60% conversion efficiency and 90% utilisation for a modern CCGT, every 10 GW of incremental gas-fired power demand will require 1.2 bcf per day of natural gas. |

LNG Export Capacity Will Remain The Prime Growth Driver in The U.S. Gas Market

To put this risked 5 bcf per day projection of on-site gas demand for data centres into context, U.S. dry natural gas production grew 4% year-on-year to a record 108 bcf per day in 2025 alongside LNG exports of 15 bcf per day.

Post-FID LNG projects in construction will generate additional U.S. gas demand of 15 bcf per day by 2031, potentially 24 bcf per day if all pre-FID projects swiftly gain FID approval.

See our 2025 year-end update for our overview of the North American LNG sector.

So, just as we last concluded in our Q324 note, risked projections for off-grid data centre-led gas demand remain extremely modest when compared to prospective LNG export capacity.

But Watch This Space - AI Compute is Migrating From Training Toward Inference

AI Training is the foundational process of teaching an AI model by feeding it massive datasets to learn patterns; AI Inference is the deployment phase where the trained model applies its knowledge to new, real-world data to make predictions or decisions. Training creates the AI model, Inference applies the AI model |

Massive AI data centres will continue to dominate the headlines, but the competitive battleground is shifting toward distributed, smaller data centres to address AI-led requests at the speed that users require.

Power-Hungry Training versus Latency-Critical Inference

AI training workloads are highly power-intensive due to the extreme computational requirements of building trillion-parameter LLM models, but insensitive to latency issues.

Hyperscalers therefore prefer to site such workloads in remote, energy-rich regions where land, water and power are readily available.

Typical AI training requirements: Power: 300 MW - 2 GW+; Latency: > 100 milliseconds

By contrast, AI inference request-based workloads demand real-time, low-latency processing but such workloads individually require far less power - the result being that inference-based workloads can be distributed across smaller, modular data centres.

Typical AI inference requirements: Power: 50 - 250 MW; Latency: < 15 milliseconds

Fast-Growing AI Inference Workloads Projected To Dominate AI Training By 2030

AI Inference is the Long Game

AI companies are necessarily shifting their focus from solely training AI models to deploying them - presumably in the hope of generating a return on their vast AI investments to date.

Demand for AI inference is growing rapidly as AI tools are more broadly accepted and adopted. Inference is expected to become the dominant portion of AI computing, overtaking training as AI applications migrate from development to production.

Within a year, according to McKinsey’s global analysis, inference workloads are projected to surpass training workloads. By 2030, inference will represent 60% of overall AI workloads.

Decentralised ‘Edge’ Data Centres Will Complement Hyperscale AI Data Centre Campuses

The rapid growth of AI inference-led workloads is the prime catalyst for ‘edge’ data centres.

‘Edge’ data centres are small, decentralised facilities that position computing resources closer to end-users or devices. Unlike distant hyperscale data centre campuses, edge data centres enable real-time applications by processing data close to source - thus addressing a critical challenge: the physical limits of network latency.

AI inference-based demand millisecond-level responsiveness: after all, a self-driving vehicle cannot await a high-latency (> 100 millisecond) round-trip to a hyperscaler’s data centre hundreds of miles away for a critical driving decision!

‘Edge’ data centres for AI inference represent a fundamental retooling of AI strategy: where to site such data centres, what scale of compute to install and how to power them. Such decisions will no doubt differ dramatically from those for hyperscale AI training campuses.

Given their different purpose and scale, decentralised ‘edge’ data centres will serve to complement rather than replace existing data centre campuses. However, it is conceivable that, as training workloads potentially wane due to diminishing returns on investment, plans for future vast data centre campuses may yield to ‘edge’ data centres.

How Will Edge AI and the Growth of Inference Workloads Influence Future Power Demand?

The lower power needs of individual AI inference workloads cited above might at first blush suggest that the migration toward AI inference will ‘cap’ AI power demand. However, fast diminishing access costs (the cost of ‘tokens’ – units of compute – has fallen by 99.9% in three years!) will no doubt see demand for inference and agentic AI mushroom, the result being an overall increase in AI-led power demand – the Jevens Paradox1.

‘Edge’ data centres will prompt a broader geographic distribution of AI-led power demand, potentially reducing critical grid bottlenecks but major equipment and labour-related supply chain and permitting bottlenecks will remain, slowing the building out of data centres and, in turn, the demand for incremental gas-fired generation capacity.

1 As technology improves the efficiency with which a resource is used, total consumption of that resource increases rather than decreases.

Edge AI Models Deployed On Smart Devices Bring Intelligence Ever Closer To Operations

‘Edge’ AI inference workloads can be taken well beyond the distributed population of ‘edge’ data centres described above. The sheer scale of compute power that now exists on a single CPU or GPU chip allows AI algorithms to be deployed directly on local devices - such as sensors, smartphones, and IoT-enabled (internet of things) devices.

The power of AI, or rather edge AI, at the very point of measurement, observation or data request enables real-time, low-latency response, analysis and decision-making, enhanced privacy and, notably, offline functionality.

Obvious applications would include autonomous drone navigation, smart surveillance, health monitoring and industrial predictive maintenance.

But let’s ask an Edge AI application to explain the merits of Edge AI, while offline?

I downloaded the Locally AI app and Gemma 4B - a 4 GB edge-optimised Google DeepMind AI model - onto my iPhone, set the phone to Airplane mode and posed the question:

‘

Why is Edge AI of growing importance?’

Here is the result - unedited, just formatted:

Edge AI addresses critical shortfalls in cloud-based AI solutions, blending speed, privacy, cost-efficiency, and scalability. Its rise is driven by: Performance & Real-Time Needs

Privacy & Security

Cost & Resource Efficiency

Scalability & Flexibility

Domain-Specific Edge AI Applications

When to Choose Edge AI vs. Cloud AI |

Edge AI | Cloud AI |

Latency is critical | Bandwidth is abundant, no need for real-time processing |

Data privacy is a priority | |

Device has limited power/storage | AI model is too large for Edge |

Application is domain-specific | Global scalability is required |

Offline capability is required | No offline constraints, compute power is a non-issue |

Bottom Line: Edge AI isn’t a replacement for Cloud AI - it’s enabling new capabilities. Edge AI is a performance and privacy-first layer that unlocks new capabilities in IoT, autonomous systems, and real-time analytics. |

Not bad for a LLM small enough to upload to an iPhone, working completely offline; by the way, I did verify the above claims in case this was all just a hallucinogenic trip by Gemma 4B!

Examples of Edge AI Applications in the Oil & Gas Industry

Data-driven decisions ensure safe, efficient operations across the oil & gas value chain, from upstream exploration and production to downstream refining. And, as with other industrial sectors, digitisation, automation and AI are fast transforming the oil & gas industry.

Oil & gas companies already routinely deploy numerous sensors alongside automation systems and are increasingly implementing AI-driven analytics to optimise production efficiency and improve asset utilisation, predictive maintenance and worker safety.

But, as described earlier, traditional cloud-based AI solutions introduce latency, security risks and network dependency, making them unsuitable for critical oil and gas operations:

Upstream oil & gas operations are often located in remote, harsh operating environments - e.g. deepwater offshore platforms, desert and Arctic drilling sites - that offer limited or unreliable cloud connectivity via satellite or low-bandwidth networks.

Oil & gas operations generate massive data volumes: SCADA systems stream a host of pressure, temperature and flow measurements; rotating equipment is monitored for aberrant vibration and bearing temperatures; gas sensors and cameras detect fugitive methane emissions and flaring events. Such large datasets, if streamed continuously to the cloud for processing, would require significant and costly network bandwidth.

Edge AI is fast emerging as a powerful alternative to cloud-based AI for oil & gas operations. Running intelligent edge AI analytics close to the asset enables intelligent, real-time, low-latency decision-making, ensuring swift identification and response to any issue that may threaten operational efficiency, asset integrity, personnel safety or the environment.

Within the oil & gas industry, Edge AI involves deploying AI models directly on sensors, cameras and ruggedized servers at remote sites (drilling rigs, production facilities, pipelines and refineries) rather than relying on distant cloud data centres.

Some real examples of Edge AI applications in oil & gas operations:

Upstream

Predictive maintenance on rotating equipment

Vibration, temperature and pressure sensors on compressors, downhole pumps and top drives stream data into an edge-AI node. Local models estimate remaining useful life and detect anomalous signatures in milliseconds - far faster than cloud-based systems - generating local work orders and alarms days before failure. The result: fewer unexpected shutdowns, extended lifespans; companies report savings of 18 - 40% in maintenance costs.

Drilling Optimisation

Edge AI models ‘at the drillbit’ gather downhole sensor data to determine spatial position and formation properties, enabling autonomous, real-time adjustments to the rotary steerable system (RSS) - the result being higher (up to 39%) penetration rates (ROP) and reduced (over 40%) high-latency surface-to-downhole downlinks. Example: SLB’s Neuro autonomous geosteering - introduced December 2024.

Computer Vision for Rig Floor Safety

Cameras on the rig feed edge‑AI vision models that detect people in danger zones, missing PPE or unsafe behaviours, triggering local alarms or interlocks. Processing video locally avoids the bandwidth and privacy issues of streaming HD feeds to a remote data centre.

Smart Well Control

Edge-AI systems monitor wellhead pressure and flow rates to automatically adjust settings, increasing yield and avoiding environmental incidents.

Methane Emission Monitoring

Edge AI-enabled cameras and sensors to accurately detect fugitive methane leaks or flare anomalies in real-time, allowing operators to fix issues immediately to meet emission targets.

Real-time Seismic Analysis

Edge AI processes seismic data on-site, reducing data transmission costs and analysis time for identifying high-potential drilling zones from months to days, while ensuring data privacy for the client.

Midstream

Real‑time pipeline integrity monitoring

Distributed edge-AI nodes along a pipeline gather pressure, flow, temperature and acoustic/vibration data. Local anomaly‑detection models recognise leak signatures, wall thinning or third‑party interference and autonomously close valves to isolate segments within milliseconds, rather than awaiting a slower remote cloud-based decision.

Similarly, edge AI-enabled ‘pigs’ can be deployed to gather and swiftly analyse acoustic, visual and conductivity data to detect and locate corrosion and cracks within a pipeline.

Edge-AI vision for leak/corrosion detection

Fixed cameras or inspection robots monitor equipment in remote or hazardous locations. Edge-AI vision models can swiftly identify stains, gas plumes, corrosion or coating damage on pipes and tanks, reducing unnecessary maintenance visits, costs and risks to personnel. Local video processing with remote transmission limited to alerts reduces bandwidth and power needs for remote locations.

Optimisation of Pipeline Terminal Logistics

Edge-AI systems at pipeline loading terminals can optimise inventory, shipping and routing schedules within pipeline constraints.

Downstream

Process optimisation

Edge-AI nodes gather and analyse DCS/SCADA data across the refinery - distillation columns, crackers etc - to compute real‑time efficiency, yield KPIs and provide or implement set‑point adjustments.

Predictive Maintenance

Compressors, fans, motors and boilers are monitored by edge-AI for early‑stage degradation, reducing unplanned downtime and allowing better outage planning.

Worker Safety, Compliance Monitoring

Cameras and wearables inside plants use edge‑AI vision and sensors to detect falls, proximity to hazardous zones, missing PPE and abnormal behaviours, generating on‑site alarms rather than relying on remote monitoring centres.

Key Benefits Driving the Adoption of Edge AI in Oil & Gas

Low Latency

Instant response to critical alerts (e.g. stopping a pump within milliseconds of a fault being detected).

Lower Bandwidth Costs

Only actionable insights are sent to the cloud, reducing expensive satellite data usage.

Operational Continuity

Systems continue to function and act autonomously even when remote connectivity is lost.

In conclusion, wherever traditional markets encounter disruption, investment opportunities abound: PillarFour continues to monitor the oil & gas market and a host of emerging energy-related technologies, services and products to identify promising trends and investment opportunities.

Download the PDF

This material is intended for information purposes only. This material is based on current public information that we consider reliable, but we do not represent it as accurate or complete, and it should not be relied upon as such. We seek to update our research as appropriate, but various regulations may prevent us from doing so.

Estimates, opinions and recommendations expressed herein constitute judgments as of the date of this research report and are subject to change without notice. PillarFour Capital Partners Inc. does not accept any obligation to update, modify or amend its research or to otherwise notify a recipient of this research in the event that any estimates, opinions and recommendations contained herein change or subsequently become inaccurate or if this research report is subsequently withdrawn.

No part of this material or any research report may be (i) copied, photocopied or duplicated in any form by any means or (ii) redistributed without the prior written consent of PillarFour Capital Partners Inc.

Website links or e-mail communications may contain viruses or other defects, and PillarFour Capital Partners Inc. does not accept liability for any such virus or defect, nor does PillarFour Capital Partners Inc. warrant that e-mail communications are virus or defect free.

This document has been approved under section 21(1) of the FMSA 2000 by PillarFour Securities LLP (“PillarFour”) for communication only to eligible counterparties and professional clients as those terms are defined by the rules of the Financial Conduct Authority. Its contents are not directed at UK retail clients. PillarFour does not provide investment services to retail clients. PillarFour publishes this document as a marketing communication and NOT Independent Research. It has not been prepared in accordance with the regulatory rules relating to independent research, nor is it subject to the prohibition on dealing ahead of the dissemination of investment research. It does not constitute a personal recommendation and does not constitute an offer or a solicitation to buy or sell any security. PillarFour consider this note to be an acceptable minor non-monetary benefit as defined by the FCA which may be received without charge.

This note has been approved by PillarFour Securities LLP (FRN 722816) which is authorised and regulated by the Financial Services Authority.